How AI Changes the Software Value Chain

The value chain climate has changed. So must software companies.

Workday spent nearly two decades solving one of the hardest coordination problems in large organizations: getting HR and finance to speak the same language. HR was its wedge, but the control point was how headcount changes flowed automatically into financial forecasts. Workday became the Governor of how large organizations planned, hired, and spent. An organism suited to its climate.

Then the climate changed. AI assistants embedded in the productivity tools employees already live in — Microsoft Copilot, Google Agentspace — can now synthesize a workforce plan by pulling HR and financial data directly, without a user ever opening Workday’s interface.

Forrester called it plainly after Workday’s 2025 annual conference: the company was executing a transformation driven by the “existential threat of AI intermediation.” Workday spent $1.1 billion to acquire an AI interface layer and opened its data model to outside standards for the first time. Workday was adapting to the changing climate.

Workday is not alone. Every control point in enterprise software was shaped in an environment now changed by AI. The question is which control points weaken in the new climate — and which ones thrive.

Accelerating pace, yet again

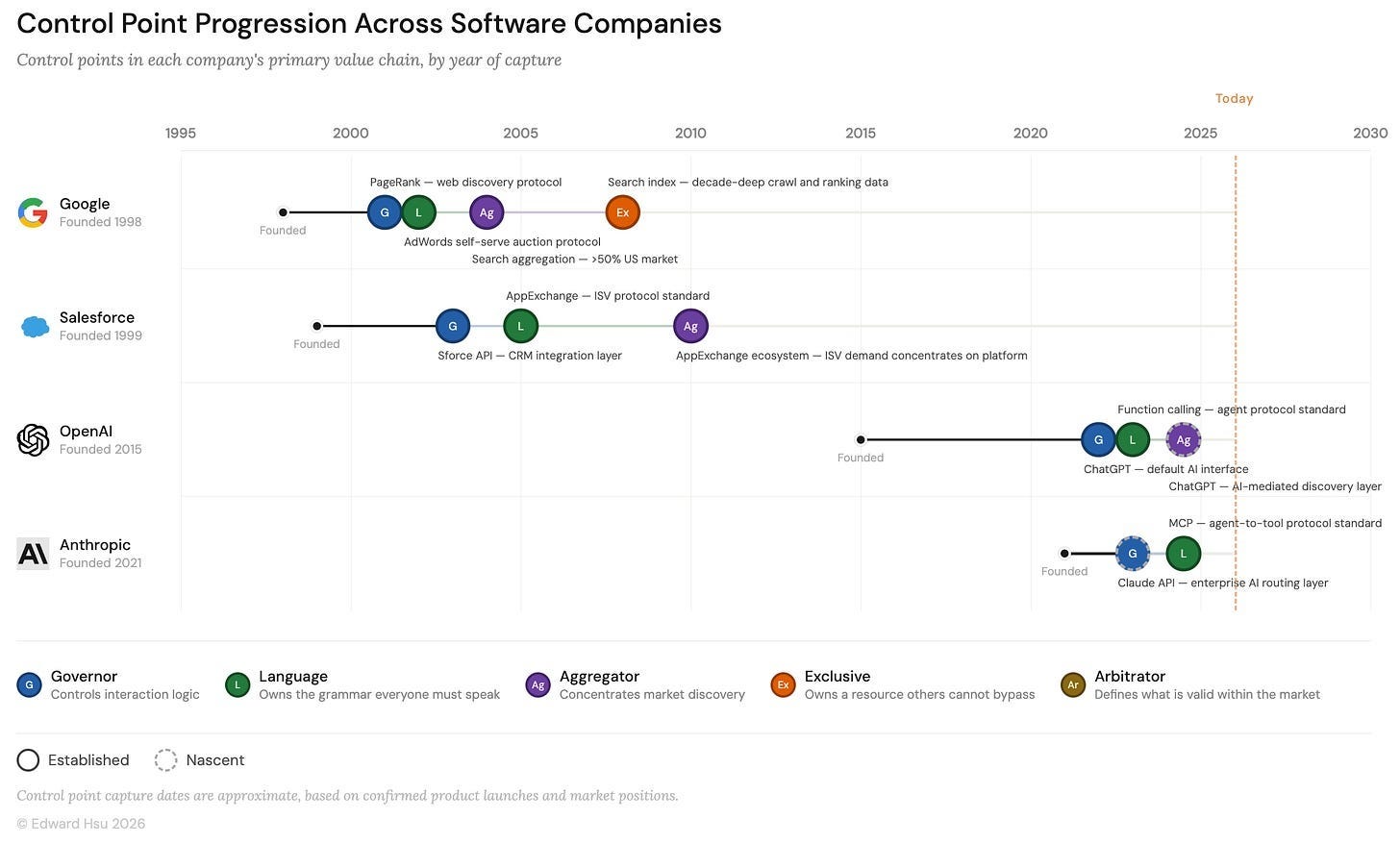

Just as the cloud accelerated the pace of innovation, AI is doing it again. Prior to AI, cloud technology cycles gave companies several years to adapt. Google took seven years between PageRank — its first control point, which defined the protocol for web discovery — and three more that followed. Salesforce took eleven. That was the pace the environment allowed. Network effects and ecosystems accumulated gradually.

AI has compressed that window in two ways. First, it lowers the cost of building both the wedge that gets you in, and the control point that gives you leverage.

Second, it accelerates ecosystem adoption — the network effects that once took years can arrive in quarters. OpenAI captured three control points in two years. Anthropic’s Model Context Protocol, the de facto standard for how AI agents connect to external tools, is a Language control point established in one year.

The chart below makes the compression visible.

The implication is uncomfortable. Control points that took a decade to establish can now be claimed in two or three years. And control points built for a pre-AI climate can be threatened in the same timeframe. The adaptation window that Google and Salesforce enjoyed no longer exists. Workday is learning that in real time.

How AI affects each control point

The five types of control points — Governor, Language, Aggregator, Exclusive, and Arbitrator — are impacted by AI differently. Below is an assessment of each.

Governor — complexity moats are dissolving, gateways to Exclusives are not

Governors control the interaction logic between value chain nodes — the routing, the authorization, the rules every participant must follow to transact. AI’s effect on Governor control points falls into two categories.

The Governors under pressure are those whose moat was complexity. Middleware platforms, iPaaS layers, and proprietary integration standards derived their structural value from the fact that connecting systems was hard. It required specialized expertise, money and time. AI is collapsing that barrier. An internal IT team, developer, or scrappy vendor can now build integrations that previously required weeks of specialized work. Platforms like MuleSoft, Boomi, and Workato built real businesses on that complexity premium. That premium is compressing.

Many SaaS companies are responding by going headless — decoupling the front-end UI from the backend logic and API layer. The instinct is correct. If AI agents are becoming the new interface, a product whose value lives only in the UI is vulnerable the moment an agent bypasses it. But going headless just keeps you relevant with AI agents, it does not get you a control point. An API layer that nobody is structurally dependent on is still a wedge, and replaceable. The question after going headless is the same one that was always there: which control point can we own?

The Governors that are not threatened are those backed by exclusive access to something genuinely valuable. Stripe governs payment flows not because integrating it is complex, but because it owns the relationships with card networks, banks, and fraud infrastructure that is difficult to replicate. Making it easier to call Stripe’s API doesn’t weaken Stripe — it strengthens it by lowering the barrier to adoption.

When a Governor is backed by an Exclusive, AI makes it more powerful, not less. Easier integration means faster adoption and deeper network effects. The companies that should be concerned are those whose Governor rested on the assumption that integration would stay hard.

Language — translation got cheap, ecosystem depth got cheaper to build on

Language control points own the protocol — the grammar every participant in a value chain must speak to communicate. The environment that made proprietary formats structurally powerful was one where translation was expensive. Conforming to someone else’s standard required certified partners, significant engineering time, and organizational commitment. That friction was the moat.

Language control points being weakened by AI are those whose power came from the cost of leaving, not the value of staying. Epic, which runs the electronic health records of roughly half of American hospital beds, built its position on proprietary data formats — the specific structure in which patient records, clinical notes, and billing data were stored and exchanged. For decades, accessing that data required certified implementation partners and significant engineering investment. Switching out was prohibitively expensive.

HL7 FHIR — the open standard that defines how healthcare data is structured and exchanged across systems — existed as an alternative for years. What changed is that building clinical tools natively on FHIR, and migrating off Epic’s proprietary layer, became economically viable once AI reduced the integration and translation overhead. The lock-in was never the format itself. It was the cost of leaving it. That cost is falling, and Epic is being pushed toward openness as a result.

Language control points being strengthened by AI are those built on open standards with deep ecosystem adoption. Anthropic’s Model Context Protocol is the clearest current example. Within a year of release it became the de facto standard for how AI agents connect to external tools, adopted by OpenAI, Google, and thousands of developers. MCP didn’t win because Anthropic forced conformity — it won because the ecosystem built on top of it, which is the only way a Language control point compounds rather than erodes.

The diagnostic: if your Language control point’s power comes from the cost of leaving your format, AI is accelerating the exit. If it comes from the density of what has been built on top of your standard, AI is deepening it.

Aggregator — being the destination is no longer enough

Aggregators concentrate demand — they are the nodes all supply must pass through to be discovered. AI’s effect on this control point depends entirely on why it became the Aggregator.

Aggregators whose power came from being the place where everything was, are directly threatened. Google’s Aggregator was built on a specific mechanism: users express intent, Google matches intent to supply, and supply competes for discovery through ranked links. That mechanism is breaking down. When a user gets a direct answer rather than a list of links, the traffic publishers and advertisers depend on stops flowing. According to BrightEdge, a search analytics firm, search impressions are up nearly 50% year over year — yet paid click-through rates are down roughly one third. Google has already rolled out AI Overviews to over one billion monthly users and began testing AI Mode in early 2025, where the entire results page is AI-generated. Google is adapting to the new climate. The alternative is losing the moment of user discovery to ChatGPT and Perplexity.

The same logic applies to any Aggregator whose value was breadth. If an AI agent can shop across Amazon, Walmart, and a dozen other vendors simultaneously, the reason to start on Amazon weakens. The agent removes the need to choose a destination.

The Aggregators that hold their position are those with something no other destination has. Amazon is the instructive case. Its fulfillment network — warehouses, logistics infrastructure, two-day delivery — is something no AI agent can route around if you need the thing by Thursday. Its decade of behavioral data on hundreds of millions of shoppers makes an agent drawing on that history materially smarter than one starting cold. So while an AI agent can find a cheaper price elsewhere, it cannot replicate what Amazon knows about you or get the package there faster.

The destination was always the visible part of the control point. But how a company became an aggregator is the difference - and AI is making that distinction impossible to ignore.

Exclusive — the load-bearing structure underneath everything else

The Exclusive control point owns a non-bypassable scarce resource. Every other control point type can be held for a time through complexity, network effects, or first-mover advantage. AI is dissolving those premiums. What remains when they dissolve is either an Exclusive underneath, or nothing structurally durable at all.

At the infrastructure layer, the scarcity is real and intensifying. Compute, specialized hardware, and the physical capacity to train frontier models are genuinely limited. NVIDIA’s position in GPU compute is the clearest current example — every major AI system depends on it.

Proprietary data generated through real-world operations is similarly durable. Two forms deserve particular attention. Behavioral data — the accumulated record of how users search, buy, abandon, and return — becomes directly load-bearing as AI agents take over more of the decision layer. The agent drawing on years of behavioral history outperforms one starting cold. Workflow context is the enterprise equivalent: the institutional memory of how a specific organization routes approvals, resolves exceptions, and structures its processes. An AI agent embedded in those workflows accumulates context no external system can replicate.

The Exclusive control points under pressure are those built on information rather than operations — documented best practices, synthesized frameworks, published methodologies. AI can surface that kind of knowledge at scale. The distinction that matters: McKinsey’s value is not that it has frameworks — it is that it has applied them across hundreds of engagements in conditions that cannot be replicated. The deeper the operational application, the more durable the Exclusive.

The diagnostic has changed with AI - it is no longer enough to ask whether you have a control point. The question is whether there is an Exclusive underneath it. AI is not destroying control points — but is favoring control point stacks that include an Exclusive

Arbitrator — the rules of the new environment are still being written

The Arbitrator defines what is valid within the value chain — the conditions every participant must satisfy to exist in the market. In a stable environment these are among the most durable control points: regulatory frameworks calcify, compliance ecosystems grow up around them, and challenging the standard becomes prohibitive.

AI has destabilized that dynamic. The rules governing valid AI infrastructure, acceptable model behavior, and compliant data use are being written now, faster than established frameworks can respond. That makes the Arbitrator unusually contestable.

The contest is happening at two levels. At the regulatory level, the EU’s AI Act represents the most serious attempt to define the rules formally. In the United States, the fight is over whether AI governance happens federally or fractures into a patchwork of state laws. NVIDIA’s Jensen Huang lobbied Congress directly in late 2025, pushing for a single federal standard. For a company whose hardware runs every major AI system, helping define what constitutes valid AI infrastructure is not a political stance — it is an Arbitrator play.

The second mechanism is technical rather than regulatory. The companies whose evaluation frameworks, safety benchmarks, and model outputs become the reference standard for AI quality are building Arbitrator control points through a different path. If your model is used to evaluate other models, you define what good looks like. That authority, once established, is self-reinforcing: the standard attracts the researchers, the researchers deepen the standard, and the standard becomes the environment every other participant has to adapt to.

What this means if you are building enterprise SaaS

The climate change argument cuts differently depending on where you currently sit.

If you hold a control point today, the first question is whether the conditions that gave it structural leverage still exist. The pattern across every control point type is consistent: the ones that compound in an AI world have an Exclusive underneath them. Behavioral data, workflow context, physical infrastructure, ecosystem depth — something genuinely unique, that the AI layer above it depends on. The ones that don’t are relying on complexity premiums, and AI is dissolving those.

Apply the sovereignty test against the conditions of the new environment, not the old one: if a well-funded competitor rebuilt your category natively on AI tomorrow, which parts of your control point would survive? The parts that would are worth doubling down on. The parts that would not are worth addressing before a faster-adapting competitor does it for you.

If you do not yet hold a control point, the narrowing window cuts both ways. The same dynamics that compressed OpenAI’s capture timeline apply to any company willing to identify the right node and move toward it deliberately.

Several remain genuinely open. The Governor control point for AI-native workflows is still being contested in most vertical industries outside the largest enterprise platforms. The Language control point for how AI systems communicate within regulated industries — healthcare, legal, manufacturing, financial services — is largely unwritten, and the Epic/FHIR dynamic is playing out in slow motion across all of them. The Aggregator control point for AI-mediated discovery remains the most visibly contested, with Google’s own restructuring of its search product the clearest signal that the outcome is not yet determined.

These openings will not stay open. The organisms best adapted to the new climate are already moving.

Interesting read, the speed of change right now is hard to compare to anything we’ve seen before.

The Exclusive diagnostic is the sharpest thing in this piece. Every

control point argument eventually collapses into the same question:

what is underneath it that AI cannot route around? Complexity premiums

are gone. First-mover advantage compresses from years to quarters.

What remains is either proprietary data, workflow context, or physical

infrastructure — and most SaaS companies, if they are honest, have

none of those. They have a UI and a switching cost. The window to build

something genuinely structural is narrowing faster than most roadmaps

are moving. Which control point type do you think most mid-market SaaS

companies can still realistically claim before that window closes?